Mat credit is rs 20.

Mat credit entitlement example.

Tax liability of a company for fy 2019 20 under normal provisions of the income tax act is rs.

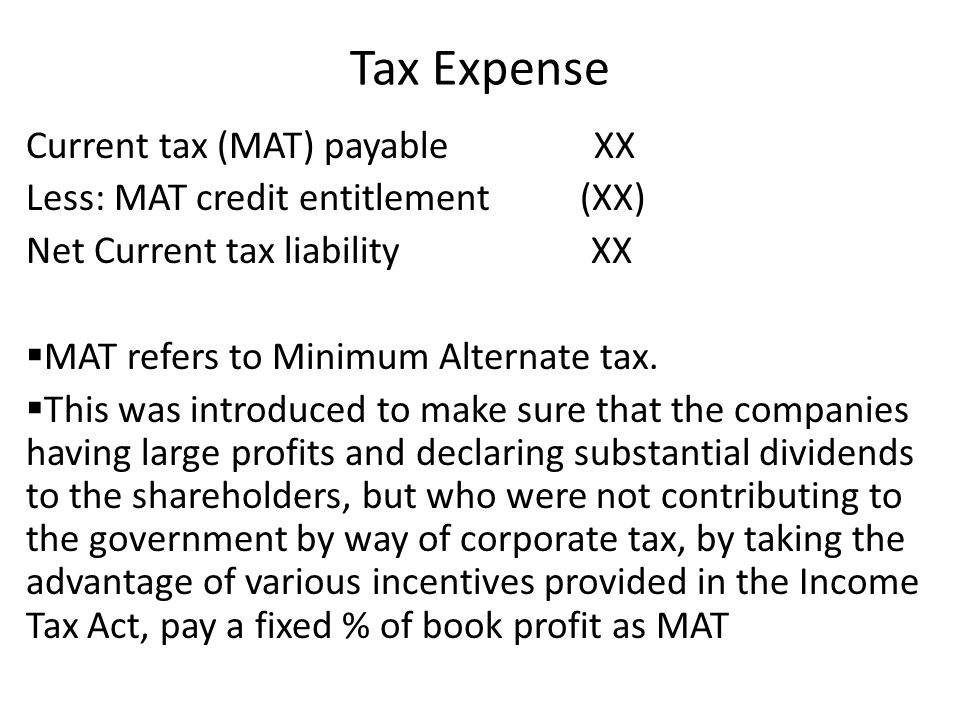

The difference arising out of mat paid and mat credit entitlement can be treated as tax paid during the year.

Provision for taxation a c dr.

The following entry is to passed mat credit entitlement a c dr.

Profit loss account.

In the above case mat credit rs.

Accounting for this credit would be made if the company is expecting to utilize this credit before it lapses in the future.

To profit loss a c cr.

Such excess of tax credit is allowed to be carried forward and set off in the financial year in which the company is liable to pay tax under the general provisions of the income tax act.

A tax credit scheme is introduced by which mat paid can be carried forward for set off against regular tax payable during the subsequent fifteen years period subject to certain conditions as under when a company pays tax under mat the tax credit earned by it shall be an amount which is the difference between the amount payable under mat and the normal tax.

Rejected the set off.

Since the company is liable to pay mat the company can avail the difference of the tax payable as per mat and tax payable as per normal provisions as mat credit.

To mat credit entitlement a c further mat credit is to be reviewed at each balance sheet date.

The cag has reviewed 182 cases in 19 states and found that in some cases there was none or minimal set off that could be claimed but the a o.

According to paragraph 6 of accounting standards interpretation asi 6 accounting for taxes on income in the context of section 115jb of the income tax act 1961 issued by the institute of chartered accountants of india mat is the current tax.

8 lakh while the liability as per the provisions of mat is rs.

It must also be noted that deferred tax charge is not covered by any other clause of the explanation to section 115jb 2 and is therefore not required to be added back in the computation of book profits for the purpose of section 115jb.

For more information on mat credit refer to this article.

The unavailed amount of mat credit entitlement if any should continue to be presented under the head loans advances.

Such tax credit shall be carried forward for 15 assessment years immediately succeeding the assessment year in which such credit has become allowable.

This is with effect from ay 2018 19 prior to which mat could be carried forward only for a period of 10 ays.

Moreover the mat credit set off can only be to the extent of the difference between the regular corporate tax and mat liability calculated.

It will be disclosed under loans and advances.

Mat credit entitlement will be treated as an asset and the accounting will be done by crediting the profit loss a c if there is a virtual certainty that the company will be able to recover the mat credit entitlement in future limited period.

100 tax as per mat rs 80 tax as per normal provisions i e.

While availing the mat credit.

Allowed a huge amount and in some cases where set off could be claimed but the a o.

While writing down the mat credit entitlement following entry is to be passed.

Rs 14 43 000 rs 12 48 000 rs 1 95 000.